Global Site

Breadcrumb navigation

Message from the CFO

We are currently making steady progress toward achieving our targets under Mid-term Management Plan 2020. An important issue is capital allocation.

With regard to the cash we generate, it is important to think about long-term business results when considering its allocation. Focusing excessively on short-term profit may lead to reduced opportunities for investment in development as well as expenses for sales expansion based on a shortsighted outlook, which is not advisable. Since my appointment as CFO, I have promoted the view within the Company that in conducting management, short-term profit is to be optimized and long-term profit is to be maximized.

I will explain our initiatives to generate cash and our approach to capital allocation, also touching on the impact of the COVID-19 pandemic.

Cash Generation

Improving profitability and increasing asset efficiency are both important for generating cash to fund the abovementioned capital allocation. Another way to generate cash is to monetize assets.

Improving Profitability

We are strengthening our profit structure so that we can continue making the investments needed to survive amid global competition. In fiscal 2019, we carried out structural reforms that reduced fixed expenses, the effect of which was reflected in our profit levels for fiscal 2020.

In terms of business portfolio reform, we decided to deconsolidate NEC Display Solutions Ltd. and convert it to a joint venture in an agreement with Sharp Corporation in March 2020. Then, in June 2020, we decided to stop accepting new orders in our global energy business. By continuing to focus on our core businesses, we will increase profitability.

Unprofitable projects weigh down on profits. Currently, we are making improvements in this area with the aim of reducing the losses from these projects from a level of more than 10.0 billion yen to less than half of that. Projects may become unprofitable if they are investments in new domains or in novel projects, or if risks have materialized due to inappropriate project management. By conducting more stringent checks from a legal standpoint, we have managed to reduce the level of unprofitable projects to a certain extent. We can improve further by strengthening early detection of risks in the upstream stages of the projects.

Increasing Asset Efficiency

In an effort to increase asset efficiency, we are promoting companywide CCC improvement measures such as implementing prepayment negotiations, ensuring appropriate cycle times and optimizing inventory levels. In fiscal 2020, we conducted a pilot project in four divisions and managed to introduce improvement measures worth over 10.0 billion yen. From fiscal 2021, we will build a cross-divisional team of several hundred people to expand these activities companywide.

Monetizing Assets

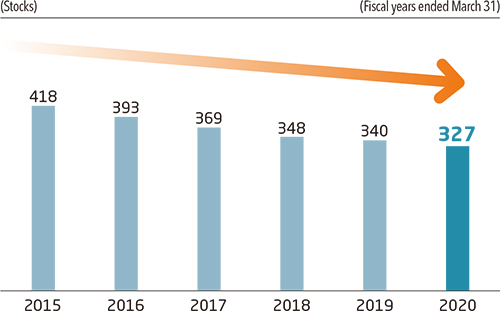

In April 2020, we decided, in principle, to eliminate cross-shareholdings. The method and timing of the sale of these shareholdings has been the subject of careful consideration. I aim to complete the sale of shares totaling at least 50.0 billion yen over the coming year or so. Cross-shareholdings will be held only when the Board of Directors has accepted the rationality of the shareholdings, having clarified their strategic value and considered the return from a capital cost perspective.

In addition to cross-shareholdings, we are also actively monetizing available-for-sale assets.

Number of Stocks Held

Market Value (Amount Recorded on the Balance Sheet)

Capital Allocation

We are making good progress with Mid-term Management Plan 2020, and steadily executing measures aimed at achieving the final-year target of an operating profit ratio of 5%. In our next mid-term management plan, we will target an even higher operating profit ratio.

To do so, I believe it will be important to allocate capital appropriately, seeking a balance between a sound financial structure, shareholder returns, and growth investments.

Ensuring a Sound Financial Structure

With regard to ensuring a sound financial structure, I believe that our balance sheet is sufficiently stable. Taking our D/E ratio and net debt/EBITDA ratio as indicators of soundness, we will allocate capital to increasing financial soundness in parallel with making growth investments with a view to raising our credit rating.

Shareholder Returns

Turning to shareholder returns, our target for the dividend payout ratio is around 30% of the average profit over the past five years. Our policy is to realize stable dividend payments to meet shareholder expectations. At the moment, we don’t plan to conduct any share buybacks. Given NEC’s current business environment, we believe that we can create greater corporate value by making growth investments such as M&As, and that increasing corporate value will result in a better return to shareholders.

Growth Investments

The main recipients of capital allocation for growth investment are R&D investment and M&As.

Our current R&D expenses account for just under 4% of revenue. Over the long term, however, we want to expand our R&D targets by raising the level nearer to 5% after increasing the profit levels of our businesses. We will discuss an appropriate level of R&D expenses for the next mid-term management plan, as we ascertain the outcomes of our investments to date.

Looking at M&As, during Mid-term Management Plan 2020, we invested around 200.0 billion yen to acquire Northgate Public Services Limited (NPS) and KMD Holding ApS (KMD). The post-management integration process for these two acquisitions is proceeding steadily, and we are beginning to see synergistic effects. In addition, these M&As have contributed significantly to growing our NEC Safer Cities business. We will continue executing M&As targeting companies that will directly boost the growth of our core businesses, to the extent that such investment does not impair our financial soundness. When making these evaluations, I think it is important that the target company has an established customer base and strong products, and the ability to stably generate cash. At the same time, we also regularly check the level of our risk assets, and maintain the ability to make investments without causing concerns over business continuity. We will maintain equity at a level that will not be impaired by events such as the recent COVID-19 pandemic.

NEC’s basic policy for capital allocation is to maintain this balance between growth investment, shareholder returns, and increasing the soundness of its financial structure.

Review of Fiscal 2020 and Financial Management in Fiscal 2021

I have explained NEC’s basic policy for capital allocation and the generation of cash to fund it. Now I will review our financial results for fiscal 2020 while explaining our initiatives for achieving our targets for fiscal 2021, the final year of Mid-term Management Plan 2020.

In fiscal 2020, we achieved tremendous year-on-year gains in both revenue and operating profit as we reaped the benefits of a series of structural reforms conducted in fiscal 2019, and each segment made improvements. Looking back over the past two years, we made advance payments for expense and structural reforms once we were sufficiently sure of achieving our internal targets. These payments totaled 15.0 billion yen in fiscal 2019 and 27.0 billion yen in fiscal 2020. We are now carrying out measures related to proposed investments for fiscal 2021 onward, improvements to the profit structure, and optimizing our assets.

Net profit totaled 100.0 billion yen, its highest level in 23 years, mainly due to improved operating profit and tax effects from completing procedures related to previously liquidated corporations. As a result, the year-end dividend increased from the initial forecast of 30 yen per share by 10 yen to 40 yen, for an annual dividend of 70 yen per share.

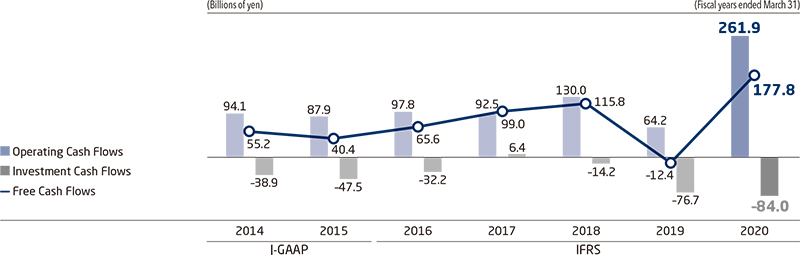

Free cash flow improved by 190.3 billion yen year on year, resulting in positive cash flow of 177.8 billion yen. This partly reflects special factors, such as an increase of around 56.0 billion yen due to changes in IFRS 16 (Leases). However, other factors included an improvement of 75.9 billion yen in adjusted operating profit (loss) and an improvement of about 36.0 billion yen in working capital due to enhanced asset efficiency. In particular, we attribute the improvement in the balance of operating income and expenditure to the gradual emergence of effects from the aforementioned CCC improvement measures.

Operating Cash Flows, Investment Cash Flows, Free Cash Flows

As I have explained, in fiscal 2020, the second year of Mid-term Management Plan 2020, we conducted investments for the future and increased our financial soundness, while achieving results that exceeded our plan for the year. In the coming fiscal year, we will strive to achieve the final year targets of Mid-term Management Plan 2020.

In these times of dramatic change in the business environment, epitomized by the recent COVID-19 pandemic, revenue levels may change rapidly and the cash outlook can easily become unclear. In such a crisis, we need to hold more ready cash on hand than in ordinary times to counter the risk of a deterioration in liquidity, thereby minimizing risk to management. We will ensure sufficient liquidity on hand by steadily procuring funds and liquidating assets. Our overseas subsidiaries experienced the impact of foreign exchange risk and foreign currency restrictions during the Asian financial crisis, and we have therefore secured borrowing facilities from banks in Japan and overseas to provide greater leeway than usual in preparation for a worst-case scenario.

In other developments, a long-standing issue over restrictions on transactions of the Company’s common stock in the United States (an order received under Section 12(j) of the U.S. Securities Exchange Act of 1934) was resolved. The restriction was lifted in June 2020. We will now communicate more actively with stakeholders in the U.S. investment market, aiming to further increase our corporate value. We will continue to realize long-term value creation and increases in corporate value through appropriate capital allocation going forward.

Message from the CFO (220KB)

Message from the CFO (220KB)